FinTake Weekly: Records Rise, Oil Retreats, and Gulf Markets Pause for Eid

FinTake Weekly from Gulf University reviews global, GCC, Bahrain, commodities, and crypto market trends for the week ending May 30, 2026.

The week of May 25–30, 2026 delivered a cautiously positive message for investors. Global equities ended stronger, helped by AI-related optimism, resilient corporate earnings, and hopes that U.S.-Iran tensions could move toward a ceasefire extension. At the same time, markets remained sensitive to inflation, interest-rate expectations, oil volatility, and holiday-shortened trading across several GCC exchanges.

Global Markets: Record Highs, But Selective Participation

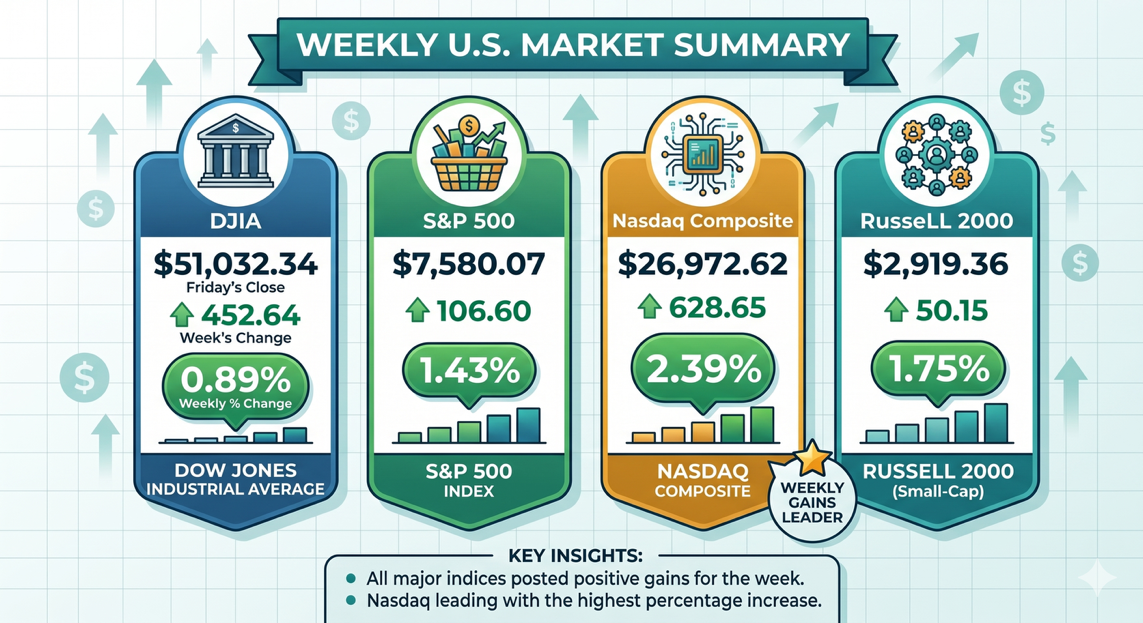

U.S. equities ended the week at fresh record highs. The S&P 500 recorded its ninth consecutive weekly gain, its longest winning streak since December 2023, while the Dow Jones Industrial Average and Nasdaq Composite also finished higher.

The rally was led by technology shares, supported by strong AI-related earnings momentum. Dell Technologies was a major driver after raising its full-year profit and revenue forecasts, which helped lift sentiment across chipmakers and software names.

Still, the market advance was not fully broad-based. Technology leadership remained strong, but several defensive and consumer-related sectors showed weakness. This suggests that investors were willing to take risk, but remained selective rather than broadly bullish.

Figure 1: U.S. Market Performance — Source: Reuters, market data, and U.S. index closing figures for the week ending May 29, 2026

Table 1: U.S. Market Performance with Weekly Change

| Index |

Friday’s Close |

Week’s Change |

Weekly % Change |

| DJIA |

51,032.34 |

452.64 |

0.89% |

| S&P 500 |

7,580.07 |

106.60 |

1.43% |

| Nasdaq Composite |

26,972.62 |

628.65 |

2.39% |

| Russell 2000 |

2,919.36 |

50.15 |

1.75% |

Table 1 is for illustrative purposes only and does not represent the performance of any specific security. Past performance cannot guarantee future results.

The key global market driver was the balance between optimism and caution. Investors welcomed signs of progress toward a possible U.S.-Iran ceasefire extension and a potential easing of shipping restrictions through the Strait of Hormuz. Lower oil prices helped reduce some inflation concerns. However, April inflation data remained elevated, keeping monetary policy risk in focus.

Gulf Markets: Peace Hopes Supported Sentiment, Eid Shortened Trading

Gulf markets entered the week with improved sentiment as investors reacted to hopes of a U.S.-Iran peace framework and the possible reopening of the Strait of Hormuz. This was important for the region because energy exports, shipping routes, inflation expectations, and investor confidence are closely linked to geopolitical stability.

Several GCC markets posted strong gains before Eid Al-Adha closures reduced trading activity. Reuters reported that Qatar rose sharply on Sunday, supported by banking strength, while Kuwait and Bahrain also gained. On Monday, Dubai, Abu Dhabi, Bahrain, and Oman moved higher as investors continued to price in de-escalation hopes.

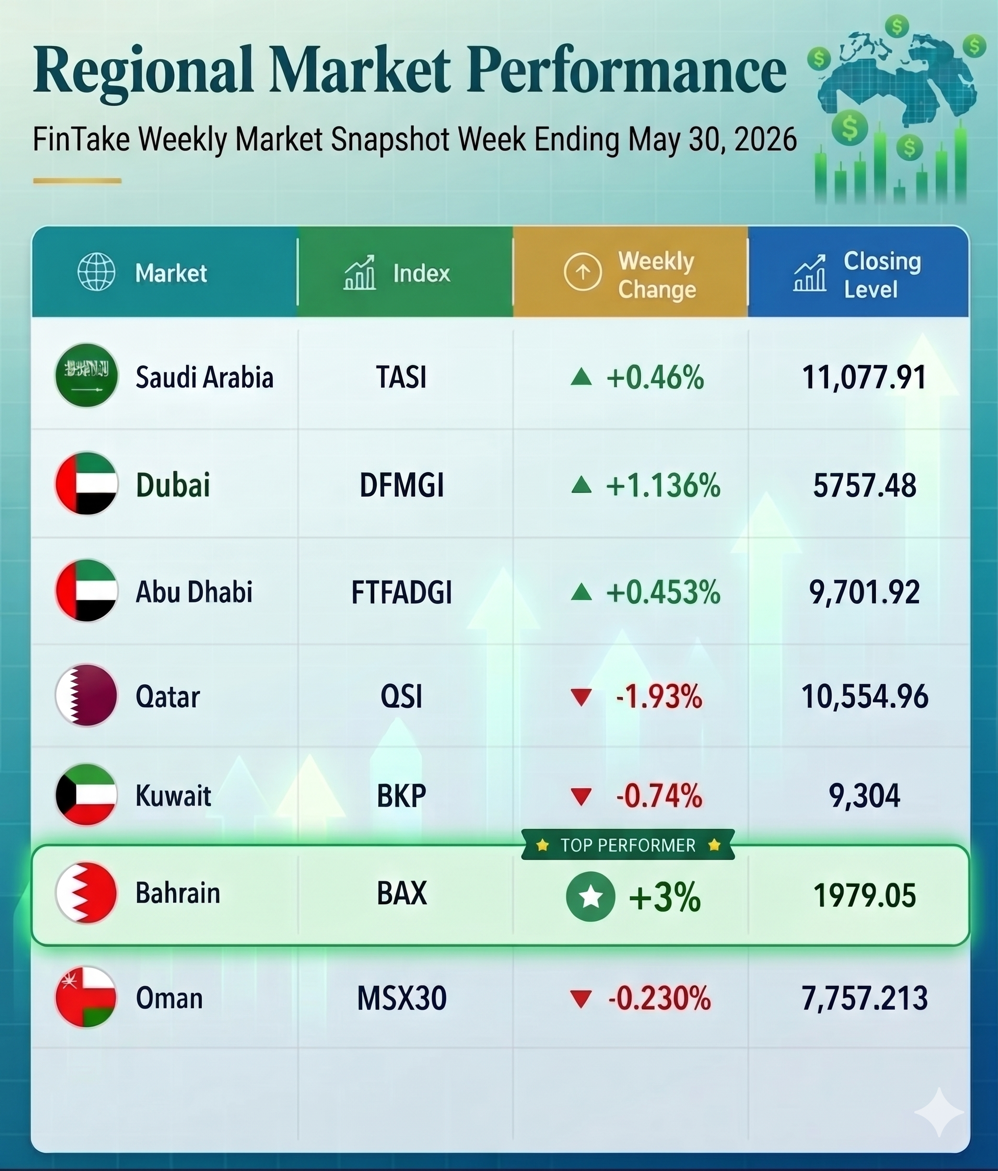

Figure 2: Weekly Performance Across Major GCC Markets — Source: Reuters, QNA, exchange holiday notices, and regional market data

Three themes shaped the regional picture:

- Geopolitical relief: Peace framework headlines supported risk appetite.

- Oil repricing: Crude prices fell as markets priced a lower probability of prolonged shipping disruption.

- Shortened trading: Eid Al-Adha holidays limited activity across Bahrain, Kuwait, Saudi Arabia, Qatar, and UAE markets.

Regional markets showed a mixed performance for the week ending 30 May 2026. Bahrain was the clear top performer, with the BAX rising +3% to close at 1,979.05, while Dubai also showed strong momentum as the DFMGI gained +1.136% to 5,757.48. Saudi Arabia and Abu Dhabi recorded modest gains of +0.46% and +0.453%, respectively, reflecting stable but limited upside. On the weaker side, Qatar posted the largest decline, with the QE Index falling -1.93%, followed by Kuwait at -0.74% and Oman at -0.230%. Overall, the regional picture was selective, with gains concentrated in Bahrain, Dubai, Saudi Arabia, and Abu Dhabi, while Qatar, Kuwait, and Oman ended lower. Because several GCC markets were closed for Eid Al-Adha, weekly figures reflect shortened trading activity and should be interpreted with that limitation in mind.

Key Takeaways

Bahrain led regional markets with a strong +3% weekly gain. Dubai showed the second-best performance, supported by a +1.136% rise. Saudi Arabia and Abu Dhabi posted smaller but positive gains. Qatar was the weakest market, falling 1.93%. Overall, regional sentiment appears selective rather than broad-based, with gains concentrated in Bahrain, Dubai, Saudi Arabia, and Abu Dhabi, while Qatar, Kuwait, and Oman ended lower.

Bahrain Bourse Weekly Market Review

Bahrain Bourse had a shortened trading week because of the Eid Al-Adha holiday. Bahrain Bourse announced that the market would be officially closed from Tuesday, May 26, 2026, until Sunday, May 31, 2026, with business resuming on Monday, June 1, 2026.

Before the closure, Bahrain’s market showed a strong upward move. The Bahrain All Share Index was last reported at 1,979.05 on Monday, May 25, compared with 1,929.48 at the previous weekly close. This represented a gain of about 3%. The Bahrain Islamic Index also improved, reaching 967.06 compared with 917.20 previously.

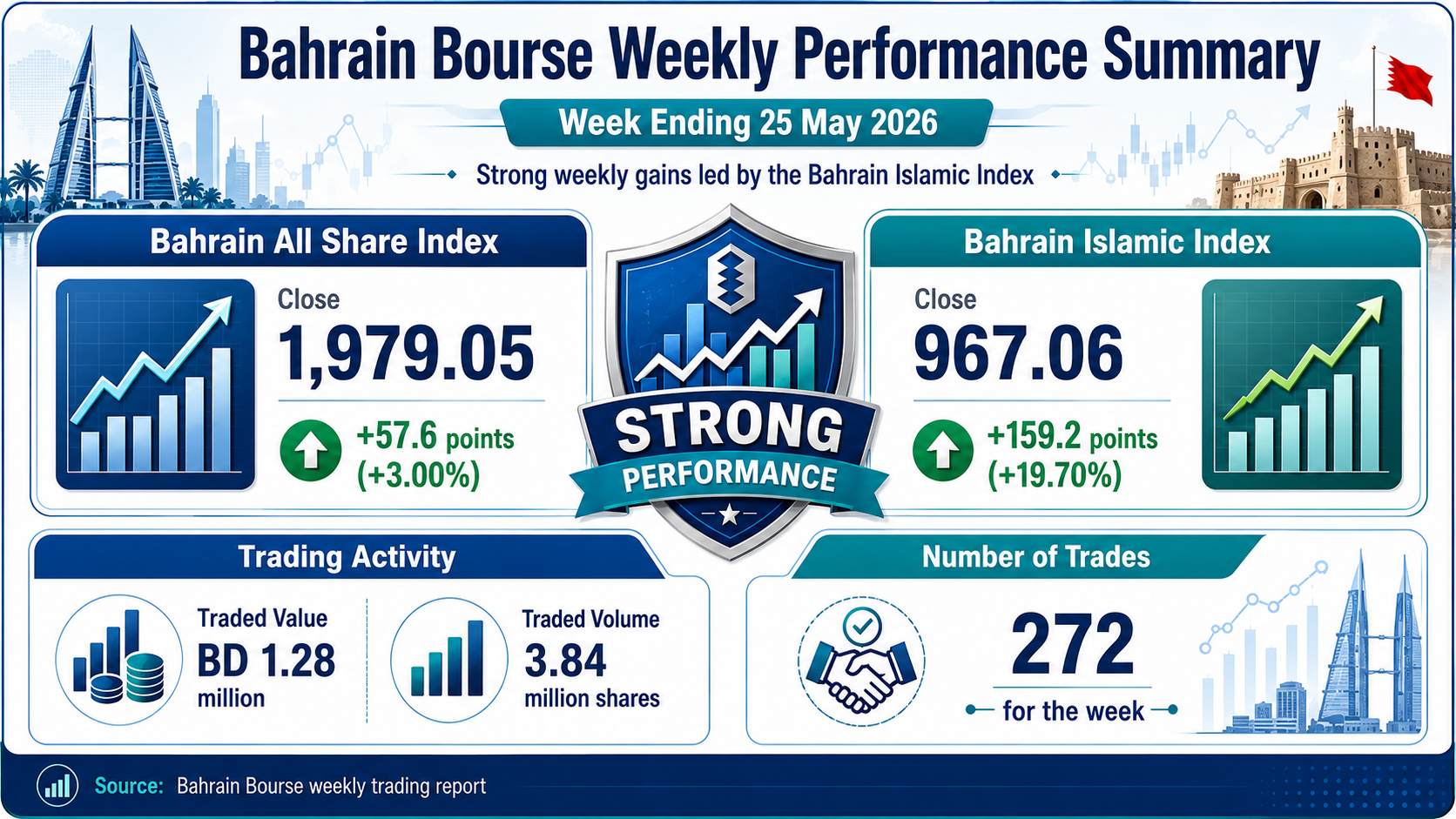

Figure 3: Bahrain Market Indices Summary — Source: Bahrain Bourse weekly trading report and market estimates for the week ending 30 May 2026

Bahrain Bourse Weekly Report Summary

Bahrain Bourse ended the week of 25 May 2026 with a strong positive performance. The Bahrain All Share Index closed at 1,979.05, gaining 57.6 points or 3.00%, while the Bahrain Islamic Index posted a sharper rise, closing at 967.06, up 159.2 points or 19.70%. This shows that the market’s headline performance was positive, with Islamic equities delivering the strongest momentum.

Trading activity remained moderate despite the strong index gains. Total traded value reached BD 1.28 million, with 3.84 million shares traded across 272 transactions. The most active securities included SALAM, ALBH, NBB, BEYON, and GFH, with SALAM leading by both traded value and volume. This suggests that market activity was concentrated in selected stocks rather than evenly across the market.

Sector performance was mixed, but gains in key areas supported the overall market. BHB Materials led the market with a 13.52% rise, helped by the strong performance of ALBH, while Financials, Industrials, and Communications Services also posted gains. On the other hand, Real Estate and Consumer Staples declined. Overall, the report shows a positive but selective market week, driven mainly by strong gains in the Islamic Index, the Materials sector, and a few active stocks.

Commodities Market Update: Oil Falls as Hormuz Risk Eases

Commodities remained closely tied to Middle East developments. Oil was the main focus as traders assessed whether a U.S.-Iran ceasefire extension could reduce shipping risk in the Strait of Hormuz.

Crude prices retreated by the end of the week. Brent crude settled near $91.12 per barrel, while U.S. crude settled around $87.36 per barrel. The decline reflected hopes that a ceasefire extension and easing of shipping restrictions could reduce the geopolitical risk premium built into oil prices.

Gold ended the week higher at around US$4,541.41 per ounce, gaining 1.02%, although it remained under pressure on a broader monthly basis. The metal continued to reflect mixed signals: investors still wanted protection against geopolitical and inflation risks, but stronger equities and changing rate expectations limited safe-haven demand.

Figure 4: Commodity and Cryptocurrency Weekly Performance — Source: Yahoo Finance, commodity market data, and crypto market data for the week ending May 30, 2026

Cryptocurrency: Bitcoin Consolidates as Regulation Develops

Bitcoin remained under pressure during the week, closing around $73,796.28 on May 29. This was lower than the prior weekend level, showing that crypto markets remained sensitive to profit-taking, macro signals, and shifting risk appetite.

Despite the weaker price action, regulatory developments remained important. U.S. regulators approved Bitcoin perpetual futures trading through platforms including Coinbase and Kalshi, marking another step in the integration of crypto derivatives into regulated U.S. market infrastructure.

The broader crypto market stayed cautious. Bitcoin traded in a consolidation range rather than leading broader risk assets, while investors watched liquidity conditions, ETF flows, inflation data, and interest-rate expectations for direction.

What Moved Markets This Week?

- AI and technology leadership supported equities: Strong earnings momentum in AI-linked companies helped push U.S. indices to record highs.

- Oil fell on peace hopes: Reports of a possible U.S.-Iran ceasefire extension reduced the geopolitical risk premium in crude prices.

- Inflation stayed relevant: April PCE inflation remained elevated, keeping Federal Reserve policy expectations in focus.

- GCC markets were holiday-shortened: Eid Al-Adha closures limited regional trading and delayed full market reaction.

- Crypto remained cautious: Bitcoin weakened, even as regulatory progress supported longer-term market infrastructure.

Key Takeaways for the Week

- Global equities ended stronger. U.S. markets closed at record highs, supported by technology strength, AI optimism, and improved risk appetite.

- The rally was selective. Technology led the market, while some defensive and consumer sectors remained weaker.

- Oil volatility eased but did not disappear. Brent and WTI fell as markets priced in potential progress on U.S.-Iran talks and Hormuz shipping restrictions.

- GCC markets benefited from de-escalation hopes. Regional sentiment improved, but Eid holidays shortened the trading week across several markets.

- Bahrain showed positive momentum before closure. The Bahrain All Share Index moved higher before the Eid break, but post-holiday confirmation remains important.

- Bitcoin consolidated lower. Crypto sentiment stayed cautious despite positive regulatory developments in U.S. crypto derivatives.

FinTake View | Global, GCC & Bahrain

Global markets ended the week with a constructive tone. Equity investors focused on AI-related earnings strength and improving geopolitical headlines, while lower oil prices helped ease some inflation concerns. However, elevated inflation data and policy uncertainty mean that the rally still depends on earnings resilience, lower volatility, and stable bond yields.

GCC markets remained closely linked to geopolitical developments and energy market expectations. Hopes of a U.S.-Iran ceasefire extension supported sentiment, but the Eid-shortened week limited trading activity. The key question for regional investors is whether optimism continues after markets fully reopen and whether oil remains stable near lower levels.

FinTake View: Bahrain’s market showed a strong pre-holiday move, supported by improved regional sentiment. With trading limited by the Eid break, investors should watch post-holiday liquidity, sector breadth, and whether buying interest remains broad enough to sustain the move.

Disclaimer: This report is for educational and informational purposes only and does not constitute investment advice. Market data reflect the latest available weekly closing figures across each market. Past performance is not indicative of future results.

Sources: Global markets — Reuters / AP market data; GCC markets — Reuters regional market reports; Bahrain data — Bahrain Bourse Weekly Trading Report, 25 May 2026; Bahrain holiday — Bahrain Bourse official notice; Oil, gold & Bitcoin prices — Yahoo Finance; Crypto regulation — Reuters; Infographics data — Yahoo Finance and Bahrain Bourse.

Weekly Market UpdateGlobal MarketsGulf MarketsBahrain BourseOil PricesInflationBitcoinFederal ReserveFinTake WeeklyGulf University

TH

Dr. Tanvir Mahmoud Hussein

Associate Professor (Finance) — Gulf University, Bahrain